Downing Street and Bond Markets

- Siddhant Nayak

- May 19

- 3 min read

How Starmer's political crisis and rising gilt yields are shaking trader confidence and threatening UK borrowing costs.

Popularity plunge for Starmer

Keir Starmer has faced a tough year so far. This includes Angela Rayner’s resignation following her failure to pay stamp duty, and the revelations of Peter Mandelson’s links with the late paedophile, Jeffrey Epstein. With the Mandelson story progressively worsening with the most recent findings

of him failing his security vetting and an inquiry for Starmer for allegedly misleading the House twice, Starmer faces a worsening approval rating, with 49% of respondents saying he should stand down as the leader of the Labour Party. To make matters worse, the recent council election failures including the astonishing loss of Wales to Plaid Cymru and loss of 1498 councillors in England has forced the resignation of four ministers in addition to Health Secretary Wes Streeting with more than 80 MPs calling for the Prime Minister’s resignation. These are all signs of an inevitable, unceremonious concession of power.

Yet, the PM has repeatedly mentioned, throughout this mess that he will continue, with his most recent announcement on the 12th of May 2026.

Traders’ anticipation

Much like the general public, traders have been on their feet, bracing for a potential leadership change. With rivals such as Andy Burnham - the Mayor of Greater Manchester who has been out of the Commons since 2017 – getting clearance to contest in the Makerfield By-Election, UK gilts have fallen after 30-year yields have risen by 0.2 percentage points to 5.85% at their highest level since 1998, causing UK borrowing costs to hit their highest level since 2008. This simple decision by the Labour party has destabilised the sterling, causing it to hit a one month low with £1 equivalent to $1.332.

Figure 2 – Source: FT Figure 3 - Source: FT

The vulnerability of the UK gilt market is also reflected in geopolitical tensions simmering in the Middle East, with no immediate signs of the war in Iran ending, leading to further uncertainty and risks of plummeting confidence in the British economy.

Why might this happen?

Like citizens, traders are very cautious of the political landscape and often apprehensive of developments in the government such as the budget as well as the scope for a new leader.

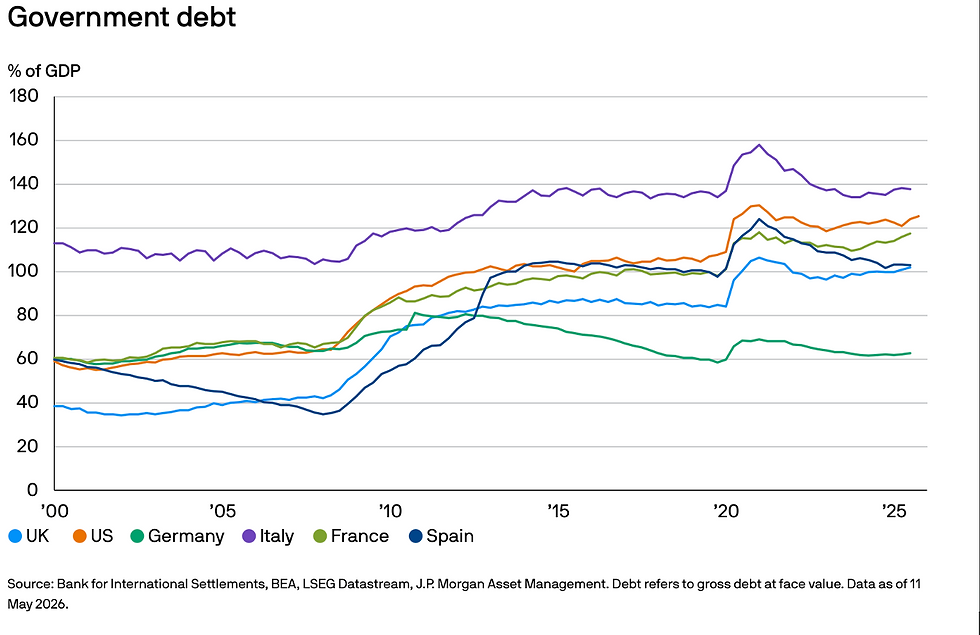

The most important factor in determining the trends of gilt yields is the government’s fiscal position. The UK has had its debt to GDP ratio rising rapidly in the aftermath of the Coronavirus pandemic as shown in figure 4 below, where it rose to nearly 110% in the peak of the pandemic, thanks to rises in government spending with the emergence of government fiscal stimulus packages such as the furlough scheme through the use of automatic stabilisers. Whilst things settled soon after that, the trend has been increasing. Albeit still being low compared to other competitor nations like Italy, the US and France, investors may lose confidence in government bonds and therefore expect a premium yield. This creates higher borrowing costs due to rising yields.

Figure 4 - Source: JP Morgan This explains why bond traders favour fiscal discipline and stable finances to guarantee the government to repay gilts and not face a debt spiral. These positions of low taxation and limited budget deficits to control spending tend to favour of the right of the political spectrum. This could perhaps explain why for someone like Starmer, who brought the Labour Party rightwards following a hard left era under Jeremy Corbyn, a risk to the leadership of more moderate with those who are more progressively left like the current Energy Secretary Ed Miliband or Streeting, can cripple confidence of traders and have effects on bond prices, with selling fuelling depreciations.

Repercussions

Rising borrowing costs may have devastating demand-side outcomes for the UK economy. Despite unexpected signs of growth at 0.6% in the first three months of the year, 29.8% of the country own property with a mortgage or loan. A potential return to a debilitating cost of living crisis, which was experienced in the peak of the Russia Ukraine war may be a fear for most ordinary households. The rise in monthly mortgage payments, alongside supply-side shocks from rising oil prices and resulting food price inflation through impacts on fertiliser supply may lead to stagflationary fears, worsening traders’ confidence in the short run. This may also lead to lower consumer confidence who will thus have a reduced marginal propensity to consume which will certainly have a negative impact on growth, therefore necessitating the need for expansionary policies to re-stimulate the UK economy such as fiscal packages to trigger further rounds of spending and aggregate demand increases in the economy.

However, the question of Starmer’s continuation of power is something that leaves those trading in the bond market on the edge of their seat.

Comments